deals

MBO at Titan Motorsport

We advised Titan Motorsport on the successful management buyout of the company.

The specialist engineering sector is expected to experience significant growth and investment in the upcoming years, underpinned by the government’s 2050 net-zero target and hydrogen fund, the HS2 rail project, and overseas interest.

Revenue streams in the sector are exposed to trends in business capital expenditure, government policy, and downstream market performance.

The government’s 2050 net-zero target will continue to pressure businesses across the UK to invest into more energy efficient machinery and equipment. A key point of interest also includes a £240m fund dedicated to hydrogen energy projects. As a result of this target, specialist engineering business should continue to see growth from the alternative energy sector, and the development and maintenance of new machinery and equipment.

Further government infrastructure investments such as the HS2 rail project, the Hinkley Point C nuclear power station, and the Lower Thames Crossing will continue to stimulate investment and revenue growth in the sector.

Market concentration in the UK is low within the specialist engineering sector. It is currently estimated that 729,000 actively trading engineering businesses employ 8.1 million people across the UK, accounting for c13% of all UK businesses and c26% of the entire workforce.[1]

Market appetite for quality control is subject to a variety of external factors such as the complexity of regulatory standards. Heavily regulated industries such as the nuclear and pharmaceutical industries have led the sector to develop engineering solutions that vary in terms of compliance levels. This is evident in specialist engineering sectors, such as fabrication, which can utilise orbital welding techniques to produce high-grade finishes for nuclear energy customers. This need to adhere to regulations encourages businesses to diversify their services using specialised teams, often in different business units.

As a result, the sector consists of a large number of small and medium-size specialised businesses serving a limited number of clients, typically in regional markets.

Reputation, quality of service, and timeliness form an essential criterion that customers look for when assigning service providers to a large project. Holding strong relationships with customers is a key competitive factor as they are likely to stay loyal to businesses that have a reliable track record.

Whilst competitiveness in the sector is less prominent than in other large sectors, such as in construction, the degree of competition has still increased over the past five years. Labour shortages, disrupted lead times, and subdued activity in several key markets, such as the automotive industries, have limited business activities.

Larger companies in the sector, such as IMI Plc, focusing in fluid industries, and GKN Ltd, an automotive specialist, have opted to consolidate smaller businesses to overcome these limitations.

There is an increasing incentive to consolidate smaller businesses in the sector, as this provides buyers with direct access to new customers and contracts in niche markets. Additionally, this gives access to greater regional market share, skilled labour, and intellectual property.

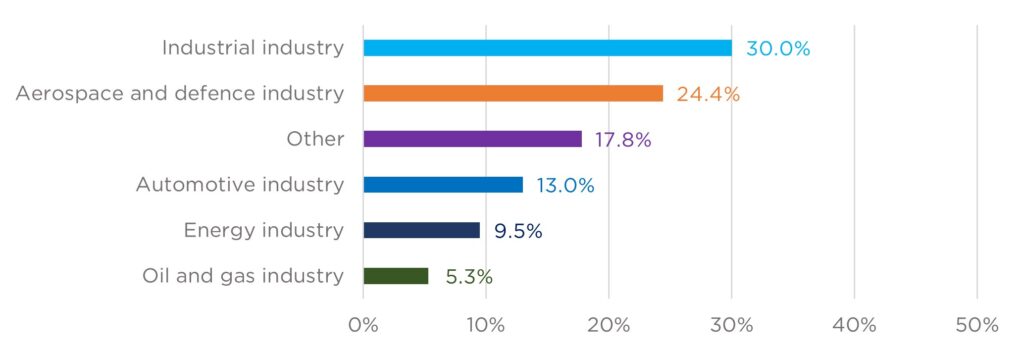

The industrial sector of the economy, which includes industries such as manufacturing, mining, and water supply, is the largest market for services, representing £2.0bn out of 2023’s total specialist engineering revenue of £6.7bn.

Efforts to improve environmental and cost efficiency have spurred demand for more lighter and more fuel-efficient equipment and machinery. Increased automation within manufacturing processes has also supported demand for precision engineered components from industrial businesses.

The easing of Covid-19 restrictions has led to the aerospace industry recovering throughout the year. As the general population becomes more comfortable with travelling abroad, the increase in flights and passengers has led to a rise in demand for maintenance and repair services.

Rapid growth in the UK’s low-carbon generating capacity has boosted demand for high-tolerance components in recent years.

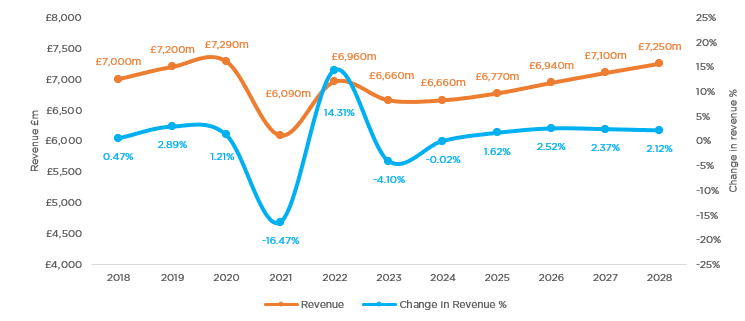

Revenue for the specialist engineering sector is forecast to increase at a compound annual growth rate of 1.7% to reach £7.3b over the five years through 2027-28.

The continued adoption of more technologically advanced and efficient machinery by firms seeking to reduce costs is expected to sustain demand for specialist engineering services. The UK’s ongoing renewables drive presents more opportunity for growth with downstream industrial and advanced manufacturing activity expected to grow in the latter part of the period as the economy stabilises, aiding a rise in business investment.

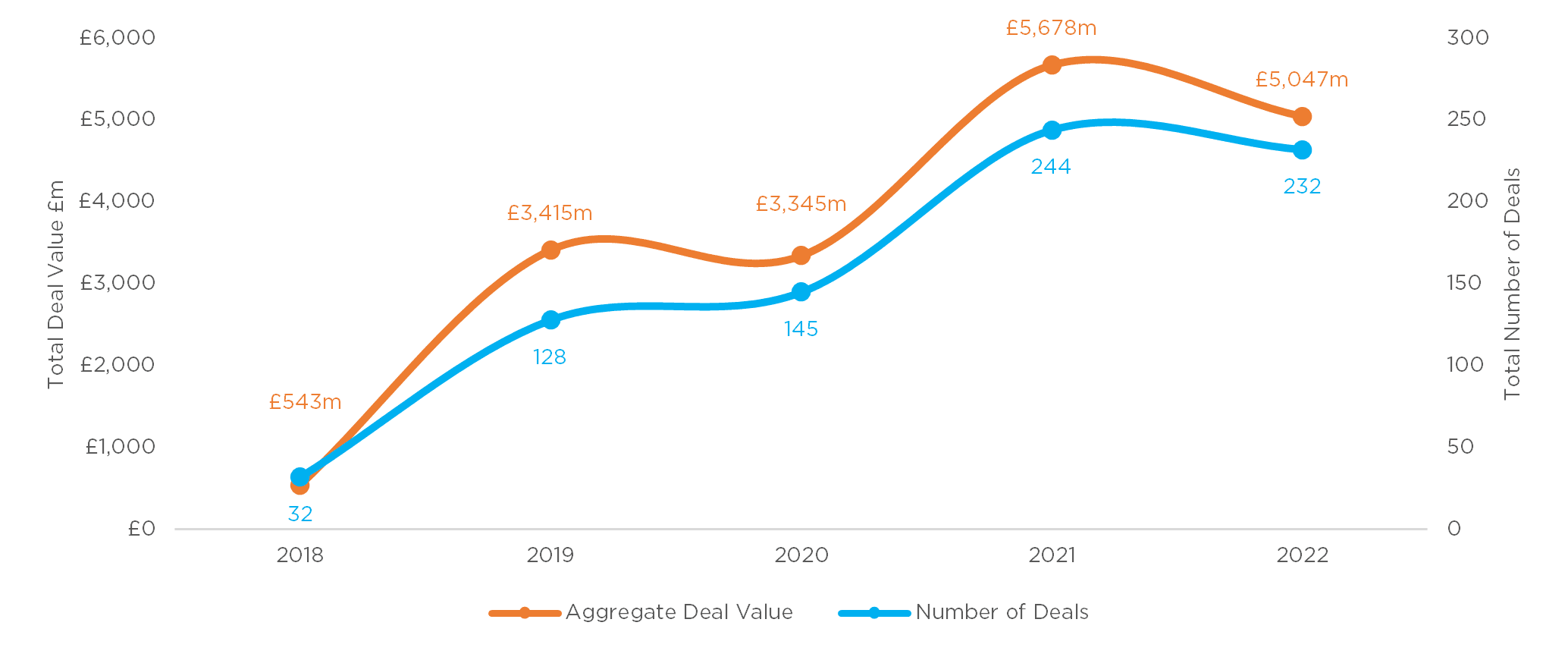

Trends suggest that now is a golden opportunity for owners of specialist engineering businesses to sell their business, with UK and European M&A activity experiencing a revival for specialist engineering businesses selling for less than £100m. The total number of deals each year has increased from 32 in 2018 to 232 in 2022. In the same time period, total deal value each year has increased from £0.5bn to £5.0bn.

With regards to the wider market, M&A activity across all sectors in the £1m-£100m range has decreased from 2018-2022. The total number of deals have declined by 20% from 1,137 to 907, whilst the total aggregate deal value has declined by 26%, from £23.7bn to £17.5bn. This demonstrates how that appetite for M&A activity in the specialist engineering sector remains robust despite economic headwinds.

The EV/EBITDA multiple is a financial ratio that compares a company’s Enterprise Value (EV) to its EBITDA (Earnings before interest, depreciation, and amortisation).

Put simply, it can be used as a benchmark for what multiple of EBITDA comparable companies are being sold for.

The gradual recovery of subdued leads times experienced in the Covid-19 pandemic, stabilised material prices, and economic stimulation has boosted M&A activity and the average EV/EBITDA multiple for UK and European specialist engineering companies in the £1m-£100m range.

In 2021, business owners selling their specialist engineering business received on average a final selling price of 7.9x their EBITDA, in 2022 this figure has grown by 3.8% to 8.1x.

In 2022, CCL Industries acquired McGavigan Holdings, a UK based manufacturer of interior automotive comments for BMW, Mercedes-Benz, and other large automotive giants. The investment team at CCL Industries used an EV/EBITDA Multiple of 8.9x to formulate a final selling price of £78.0m.

In the same year, Eladapoint acquired JS Burgess Engineering, a Derbyshire based bespoke metal stillage manufacturer for £30.0m. Demonstrating and EV/EBITDA multiple of 8.9x.

| ||

Sale of 80% of Supply Plus, a designer and manufacturer of safety and fuel delivery equipment, to Lager Crantz. | Succession Buyout of Laser 2000, a major distributor of high-end photonic products. | MBO of Titan Motorsport, a designer and manufacturer of steering, suspension and engine components for use in the automotive industry. |

| ||

| Sale of Chell Instruments to SDI Group. The business designs, tests, and manufactures high-tech instruments that measure and control gas pressures and flows. | Sale of Young Calibration, a specialist in the areas of flow meter calibration, air velocity measurement and thermal systems, to NMi in the Netherlands. | MBO of Independent Project Engineering, a designer and supplier of hardware and software solutions to global radio and television studios. |

Selling your specialist engineering business is an important life decision. Here at PEM Corporate Finance, we will provide you with expert advice and support at every step of the process.

If you would like to discuss further, please get in touch with one of our senior advisors today to arrange your free consultation.