deals

MBO at COEL

PEM Corporate Finance acted as lead adviser to COEL on their management buyout (MBO) in 2021.

The construction sector has been a prominent feature of the UK’s business landscape for centuries. The UK economy is highly diversified, with significant contributions from a range of sectors including manufacturing, industrials, healthcare, technology, and education, all of which depend on construction services to function and expand. This has kept construction firmly relevant throughout the country’s evolution.

Despite this, the construction sector has been through an eventful few years in terms of cost and revenue, due to a range of both global and local factors. Whilst there have been challenges, however, not all of the changes are negative: one of the results of this period has been a rise of Management Buy-Outs and Buy-Ins (MBOs & MBIs), leading to exciting prospects and new growth within the sector.

In this climate of opportunity, it is important to know the ins and outs of this profitable, if currently strained, sector. Read on to learn more about what has changed, why and how companies are responding. If you are a construction sector business owner considering a new business strategy, or even a buy-out or exit strategy, then find out how PEM Corporate Finance can help you.

There are two main branches to the UK’s construction sector: the residential construction industry, and the commercial side.

The residential industry covers contractors and businesses hired to undertake new builds, renovations, conversions, and repairs to residential buildings, whilst the commercial industry includes non-residential projects such as schools, hospitals, stores and airport buildings. This commercial side will cover both private and public work, as will the residential side, but residential will lean more notably towards private.

![]()

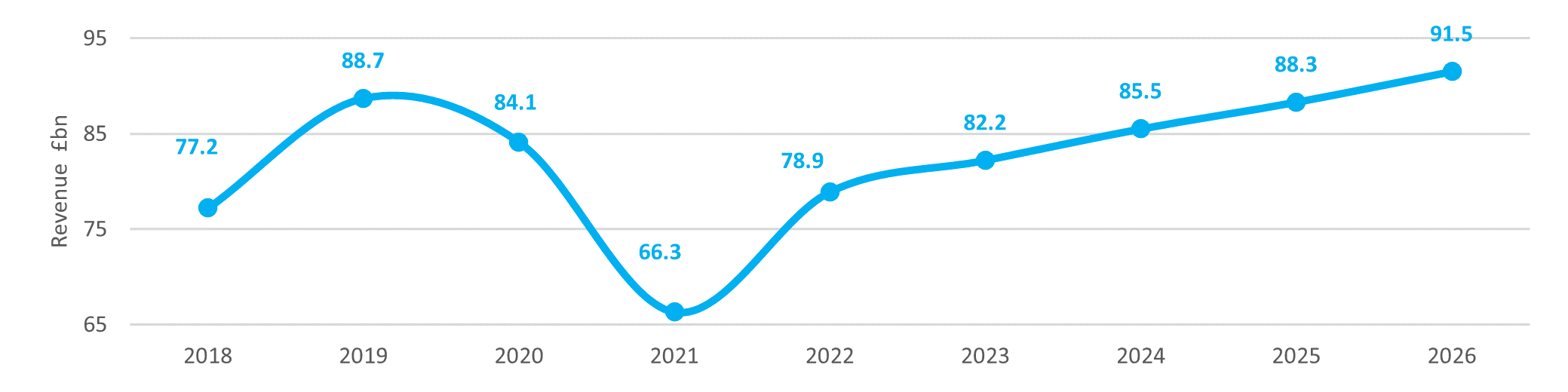

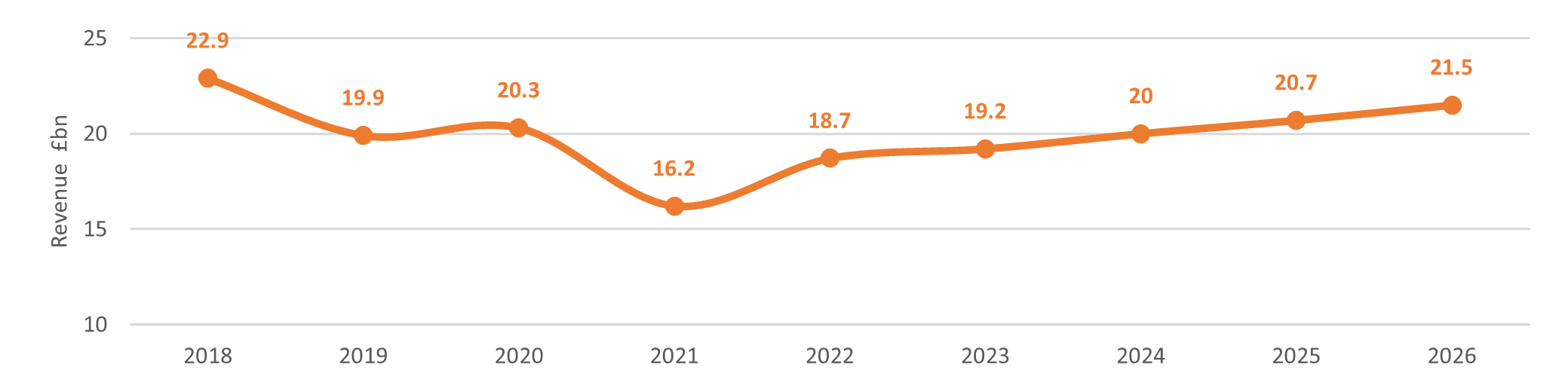

When the country’s economic or politic situation changes, these two sides of the industry are impacted differently. According to the National House Building Council (NHBC), approximately 1.4 million new homes were registered to be built across the UK market over a 10-year period, 2009 to 2019, leading to a revenue of c.£88.7bn for 2019. However, at the same time, the commercial industry experienced a downturn to c.£19.9bn in 2019 due to post-referendum operational uncertainties in key downstream markets.

In 2020 and 2021, commercial revenue decreased significantly from the 2018 high of c.£22.9bn, to c.£20.3bn and c.£16.2bn respectively. The coronavirus pandemic sent ripples through global supply chains, making materials more difficult and expensive to import. This was largely due to business activity being restricted by strict regulations imposed to prevent transmission of the COVID-19 virus. Disruptions to workflow and a subsequent decline in new housing projects led to residential revenue taking a sharp decline from the high in 2019 of c.£88.7bn, to c.£84.1bn and c.£66.3bn in 2020 and 2021.

From now until the mid-2020s, the government plans to add an extra 300,000 dwellings to the housing stock per year. Schemes such as “Help to Buy” have been vital to stimulating demand to reach this goal. This target, as well as the easing of pandemic regulations, led to the residential industry rebounding in 2022. Revenue grew to c.£78.9bn, a c.19% increase from the previous year. And the commercial industry followed a similar path, reaching c.£18.7bn in revenue – a c.15% increase.

Whilst revenue is on its way back to pre-pandemic highs, profit margins have declined due to higher costs. This can largely be attributed to further supply chain disruptions caused by the Russian invasion of Ukraine and the subsequent crossfire of global trade limitations. According to data from the Office for National Statistics, the materials price index for all construction work increased by 15.5% in October 2022 compared to October 2021. This is the result of the cost of gravel, sand, clays, and kaolin increasing by 56.7% over the year.

The long-term growth of revenue within the residential and commercial construction industries is anticipated to be led by the recovery of global supply chains, rising demand, government assistance for housing, and the demand for modernised flexible office solutions. Forecasts suggest that the residential construction industry will grow at a compound annual growth rate (CAGR) of c.3.8%, leading revenue to c.£91.5bn in 2026. Similarly, the commercial construction industry is expected to grow at a CAGR of c.3.5%, leading revenue to c.£21.5b in 2026.

Buyers and investors are looking to the sector are able to consolidate strong companies that have survived the recent harsh economic conditions, and to secure an early ticket to the benefits that come from the recovery of supply chains and trading.

In 2020 and 2021, commercial revenue decreased significantly from the 2018 high of c.£22.9bn, to c.£20.3bn and c.£16.2bn respectively. The coronavirus pandemic sent ripples through global supply chains, making materials more difficult and expensive to import. This was largely due to business activity being restricted by strict regulations imposed to prevent transmission of the COVID-19 virus. Disruptions to workflow and a subsequent decline in new housing projects led to residential revenue taking a sharp decline from the high in 2019 of c.£88.7bn, to c.£84.1bn and c.£66.3bn in 2020 and 2021.

From now until the mid-2020s, the government plans to add an extra 300,000 dwellings to the housing stock per year. Schemes such as “Help to Buy” have been vital to stimulating demand to reach this goal. This target, as well as the easing of pandemic regulations, led to the residential industry rebounding in 2022. Revenue grew to c.£78.9bn, a c.19% increase from the previous year. And the commercial industry followed a similar path, reaching c.£18.7bn in revenue – a c.15% increase.

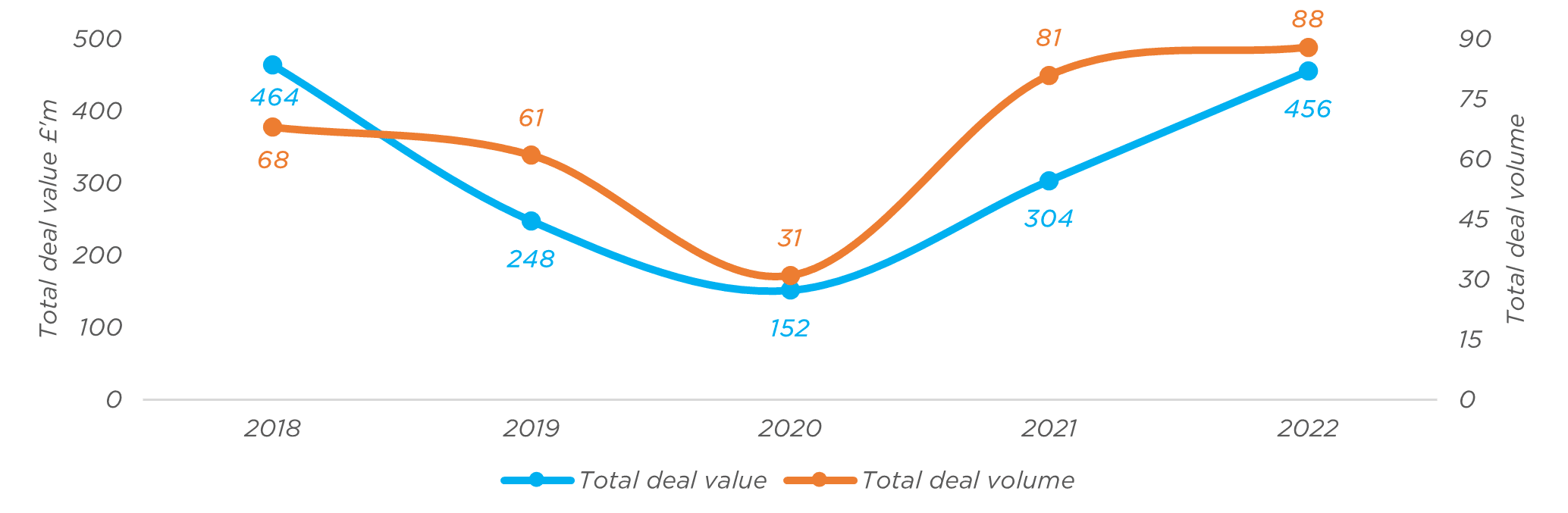

In 2020, incoming Brexit regulations and the pandemic led to disruptions in supply chains and uncertain trading expectations. Investments in the construction industry therefore appeared to be of a high-risk nature. As the general appetite for risk was low at this time, buyers and investors decided to decrease their engagement in the sector. The total deal value in the sub-£100m category took a plummet of 68% from the high of c.£464m in 2018 to c.£152m in 2020.

Following the peak of the pandemic in 2020, there was an increase in distressed merger & acquisition activity within the UK, with buyers and investors looking to acquire struggling businesses. This led to a strong recovery where total deal volume surpassed pre-pandemic levels as volume reached 88 in 2022, a c.183% increase from the low of 31 in 2020. Total deal value followed a similar trend as it rose to c.£456m.

Navigating a market with so many factors in play can be challenging, and with key corporate and financial decisions at stake, it helps to seek professional advice.

At PEM Corporate Finance, we have developed a wealth of knowledge and experience from a wide scope of construction management buy-outs (MBOs) and sales. Amongst these include the MBO of leading office design and fit-out specialist, COEL; the sale of building facades contractor English Architectural Glazing to Elaghmore; the MBO of the largest independent crane supplier in the country, Falcon Cranes, and the sale of multi-disciplinary architectural, building surveying and project management practice ATP Architects + Surveyors to RSK Group.

If you are seeking financial advice for your construction company or business, whether you are planning a Management Buy-In or Buy Out, want to discuss an exit strategy or are seeking other guidance and advice, arrange a call with us today and find out how we can help.