deals

Succession buyout of life sciences consulting firm

PEMCF advised clients, a life sciences consulting firm, on their succession buyout.

The UK healthcare and life science markets have evolved to become one of the largest in the world. Between them, they span a range of subsectors including life sciences, biotechnology, pharmaceutical, and medical care.

Over the past 10 years, the healthcare and life science sectors have become a safe haven for investors. Pressures created by an ageing population and the recent Covid pandemic have driven an increasing need for research and development facilities, whilst catalysing the growth of medical organisations.

Source: IBISWorld

UK Government healthcare expenditure is forecast to be c.£185bn for 2023, and is anticipated to grow at a 4.3% Compound Annual Growth Rate (CAGR) through 2018-25. Steady population growth and increased societal demand are expected to contribute to a widened budget for healthcare in the UK.

Aided by increased Government spending and demographic changes, there have been positive trends in the market valuations and revenues of businesses across all subsectors of healthcare.

The UK biotechnology sector, which creates products and applications using biological systems, is valued at c.£19.8bn in 2023 with a forecast CAGR of 12.2% through 2023-28. Biotechnology companies researching diagnostic techniques and human health products benefitted from a rise in private and Government funding post-Covid, raising a record c.£4.5bn of investment in 2021 and increasing industry revenues by c.15% during 2021-22.

The UK pharmaceutical wholesaling sector is valued at c.£51.8bn for 2023, exhibiting a CAGR of c.6.3% through 2023-28. However, during 2018-23, rigid regulation slowed market growth to -0.7% CAGR. This reflected Government legislation and the loss of patent protection for several high-profile drugs, which boosted generic pharmaceutical products and created downward pricing pressures within the industry.

UK medical practices, which includes general practitioners, is currently valued at c.£15bn in 2023, with a CAGR of 3.5% anticipated through 2023-28. This growth is expected to be supported by Government plans to boost NHS funding and increase available GP appointments by 50 million a year by 2024 (c.242m appointments in 2019).

In 2021, the UK Government exceeded budgeted healthcare expenditure by c.29%. The Covid pandemic directly contributed to this happening, as the government committed emergency funds to combat the spread of the virus and assist those with immediate health risks.

In 2022, funding for health services in England reduced by 1.2% as Covid-related pressures began to subside. However, forecast expenditure is expected to rise by c.2.4% through 2023-25, according to the King’s Fund.

Post-Covid, changing demographics are also contributing to growth across the sector. These include:

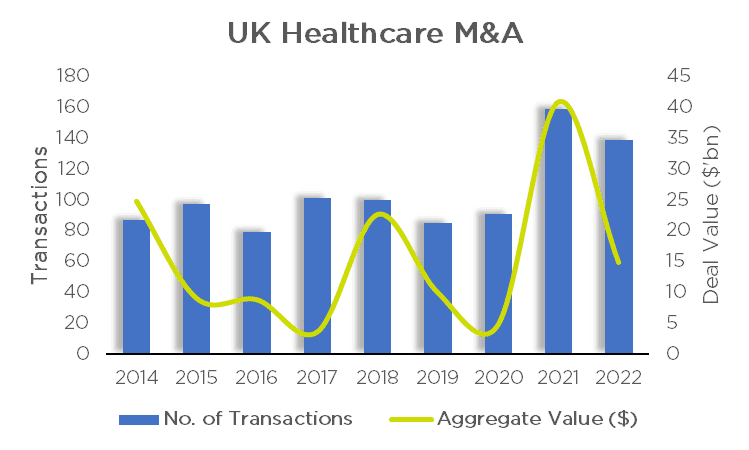

Healthcare and life sciences firms have been utilising bolt-on acquisitions to acquire specialist technology and Intellectual Property (IP) developed by smaller niche companies, with the Covid pandemic acting as a catalyst for investors and large-cap medical companies. In 2021, the UK pharmaceutical, medical, and biotechnology sectors saw deal activity reach c.160 transactions, worth over c.$40bn, which was c.75% higher than in 2020.

Source: White & Case M&A Explorer

Despite reduced deal activity in 2022, the number of transactions in the lower-mid market ($5m-$99m deal value range) increased by c.15%, displaying a growing appetite for the acquisition of relatively smaller medical firms.

Subsectors of the UK health and life sciences industries are heavily interlinked, with each division often competing for Government funding, as well as external factors (such as the Covid pandemic) influencing the prioritisation of developments. The UK healthcare sector remains strong, receiving perpetual and growing funding from the Government as a result of societal pressures, as well as significant economic growth opportunities through research and development.

Our offices are located in central Cambridge – a city recognised for its strength in knowledge-led businesses, located in one of the largest life sciences and healthcare clusters in the UK.

PEM Corporate Finance has a wealth of experience advising businesses in the UK life science and healthcare sectors. Recent transaction highlights include the sale of:

More details on our recent transactions in the sector can be found on our website here.

If you are looking to sell your business or would like a call to discuss what we are seeing in the market and how it may impact your company,

Sources include: IBISWorld, MarktoMarket, Statista and The King’s Fund